When you pull the live data on the tokenized asset market, the first thing you notice is that gold won.

Not a stablecoin. Not a government bond fund. Not a tokenized share of a company you recognize. Gold. Tether Gold and Paxos Gold together hold more than five billion dollars in the tokenized asset market right now. The narrative says tokenization is the future of finance. The data says the future of finance is, for the moment, mostly a better way to hold a metal humans have trusted since before recorded history.

That is worth sitting with before we get to the more interesting parts.

Key Takeaways:

The total tokenized asset market is $26.5 billion across 124 protocols — large in nominal terms, almost nothing against the markets it is meant to replace.

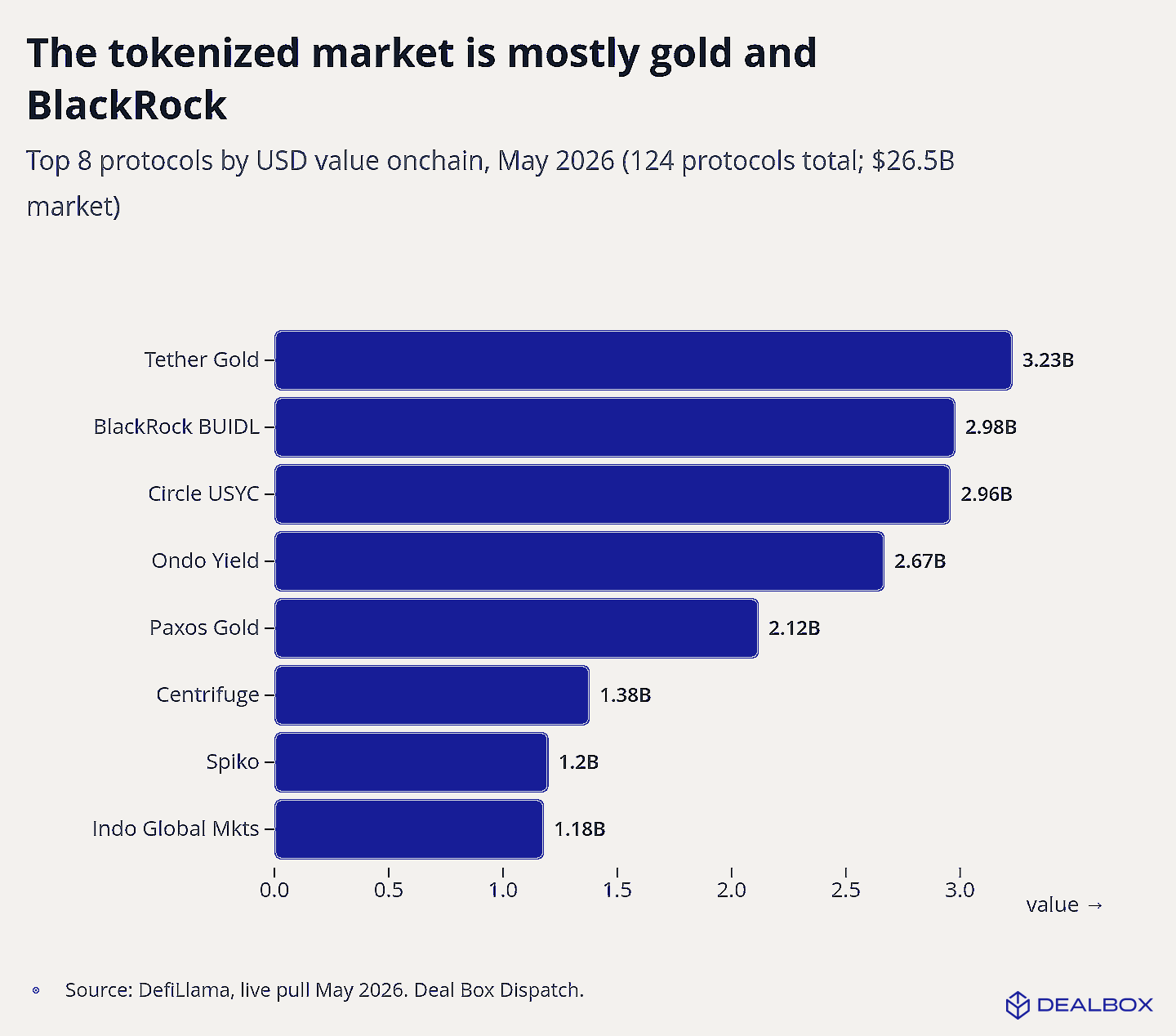

Tokenized gold leads the market at over $5 billion, ahead of BlackRock's BUIDL fund at $2.98 billion.

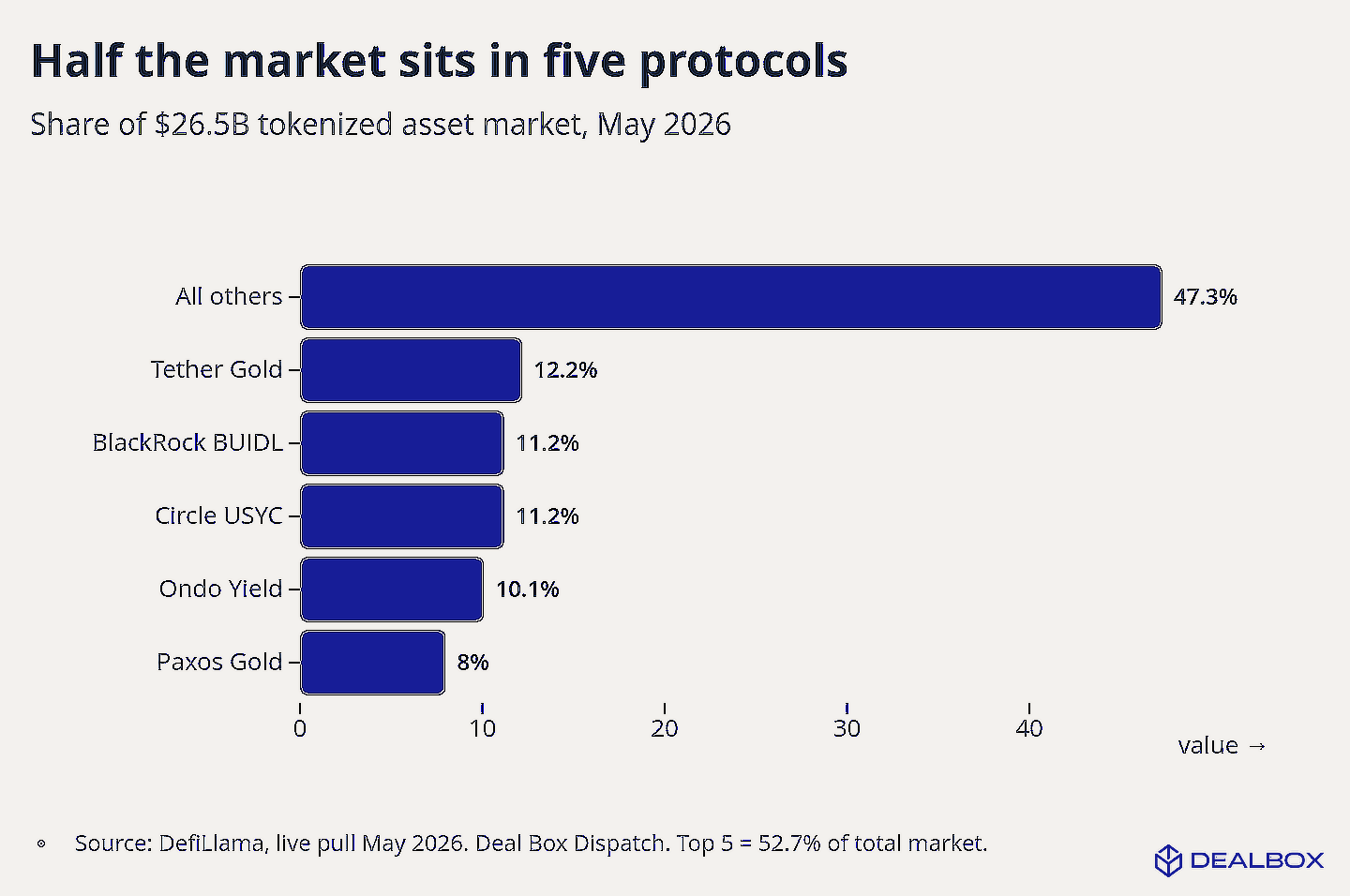

Five protocols account for 53 percent of the entire market.

Tokenized equities barely register at roughly $1.5 billion — the thing both retail and institutional investors say they want is almost entirely absent.

The SpaceX pre-IPO contract on Hyperliquid traded $33 million on its first day and crashed 45 percent on May 28. It holds no SpaceX shares. It is a leveraged bet, not equity ownership.

The infrastructure for real capital formation onchain is mostly still to be built.

The leaderboard no one expected

We pulled the live numbers from DefiLlama this week. The full tokenized asset market sits at $26.5 billion across 124 protocols as of May 2026. That number is real, and it is growing. It is also small when you set it against the markets it is meant to transform. Against the global equity market, it rounds to almost nothing.

The leaders are not who the headlines suggest. Tether Gold sits at $3.23 billion. Paxos Gold adds another $2.12 billion. Together, the two gold products account for roughly a fifth of the entire market. BlackRock's BUIDL fund sits second among individual protocols at $2.98 billion, already running on Ethereum, Solana, and Aptos. Circle's USYC follows at $2.96 billion. Ondo Yield at $2.67 billion.

The market is also more concentrated than most accounts acknowledge. Five protocols account for 53 percent of it. Everything else divides the remaining half.

Gold leading a tokenization leaderboard is a useful corrective to the dominant narrative. Tokenization is often described as the mechanism that will finally bring institutional capital into digital assets, starting at the top of the market with pre-IPO giants, government treasuries, and large corporate bonds. The data shows something different. The things that have actually tokenized well are the things that were already portable, already globally trusted, and already had a straightforward custody and settlement story. Gold qualifies. Most equities do not.

What BlackRock actually did

BlackRock's decision to run BUIDL across three chains matters more than the headline number suggests.

The largest asset manager in the world does not pick infrastructure casually. When BUIDL went live on Aptos alongside Ethereum and Solana, it was institutional money making a public choice. The fund now holds $2.98 billion in tokenized US Treasury exposure, paying yield to holders daily, with same-day liquidity available through a Circle USDC redemption facility.

That is a real product doing a real job. What it tells us is that the category of tokenized yield-bearing assets is working. Tokenized money-market exposure and short-duration fixed income have product-market fit. They solve a real problem for on-chain treasuries and DeFi protocols that need dollar-denominated yield without leaving the chain. That problem existed, the product solves it, and the market responded.

Tokenized equity is a different problem entirely.

The SpaceX contract and what it actually was

On May 18, 2026, a developer called Trade.xyz launched a SpaceX pre-IPO contract on Hyperliquid, built on its HIP-3 perpetual framework. It traded $33 million on its first day. The chief executive of ICE, which owns the New York Stock Exchange, said publicly the market could end up larger than Nasdaq.

On May 28, the contract fell 45 percent, liquidating $1.5 million in positions in a single session.

It is worth being precise about what that contract was. Trade.xyz holds no SpaceX shares. The contract is a synthetic perpetual. A leveraged bet on a price derived from secondary market trades in SpaceX equity, with no ownership, no shareholder rights, and no capital reaching SpaceX. When it crashed, what unwound was leverage, not equity. The people who lost money were not SpaceX shareholders. They were traders who had borrowed to hold a position on the direction of a price.

That distinction is not a technicality. It is the whole point.

The appetite the SpaceX contract revealed is genuine. Millions of people want access to pre-IPO companies they cannot legally own through conventional channels. They want it badly enough to take a leveraged synthetic bet on the price. The infrastructure the contract used to express that appetite is exactly what the formation layer is not.

The formation gap

Tokenized equities barely register in the current market. Real ownership of real companies onchain, with capital actually reaching those companies, sits at roughly $1.5 billion across the entire market. Against the $60 trillion-plus in global public equity it aims to complement, that number is the gap.

The gap is not a failure of demand. The SpaceX episode confirms that demand is large and growing. The gap is a failure of infrastructure.

What the formation layer requires is harder to build than a perpetual contract. It requires accreditation verification at the individual investor level. It requires a regulatory structure that allows the equity to be sold without triggering broker-dealer registration. It requires a data room that satisfies the diligence obligations of the platform, not just the curiosity of the buyer. It requires subscription documents, KYC, and a cap table that survives the offering. And it requires a technology layer that handles all of this without turning the investor experience into a compliance obstacle course.

None of that is unsolvable. Most of it has been solved in specific cases. What does not yet exist at any real scale is a platform that assembles the whole stack, runs it for US-domiciled issuers, and makes the accredited investor experience something better than a stack of PDFs and a wire instruction.

Trading a name and forming capital are different activities. The first one is busy. The second one is mostly still to be built.

What comes next

Here is the thesis.

The tokenized asset market will continue to grow, and it will continue to surprise. Gold will stay near the top of the leaderboard longer than most people expect, because it is the oldest portable store of value and the custody story is cleaner than most equities. Tokenized yield products will grow as on-chain treasuries scale. And the equity category will eventually close the gap, because the demand is undeniable and the regulatory environment is shifting.

When it does, the platform that wins the formation layer will not be the one that moves fastest. It will be the one that built the compliance infrastructure first, earned the issuer trust before the category got crowded, and assembled a track record of completed raises before anyone was watching.

We have been running that infrastructure since 2016. Sixty-six completed engagements. Zero broker-dealer fees, by structure, ever.

The formation layer is the part we work on.

FAQ

What is the total size of the tokenized asset market today?

As of May 2026, the tokenized asset market totals approximately $26.5 billion across 124 protocols, based on a live DefiLlama pull. That figure is growing but remains a small fraction of the broader markets it aims to transform.

Why is tokenized gold leading the market?

Gold has the simplest custody and settlement story of any asset class, is globally trusted, and translates well to a tokenized format. Tether Gold and Paxos Gold together account for more than $5 billion, making gold the largest single category in the tokenized market.

What is the difference between the SpaceX Hyperliquid contract and actual equity ownership?

The Hyperliquid contract is a synthetic perpetual, a leveraged bet on the price of SpaceX shares derived from secondary market trades. It carries no ownership rights, no shareholder rights, and no capital reaches SpaceX. Real equity ownership requires accreditation verification, a regulatory structure under US law, subscription documents, and capital that reaches the issuing company.

What is the formation layer?

The formation layer is the infrastructure that allows genuine equity to come into existence onchain, with real ownership, under US regulation, where the capital reaches the company rather than a trading pool. It requires accreditation verification, compliant subscription documents, a regulated platform structure, and a data room that satisfies diligence obligations.

How does Deal Box fit into this?

Deal Box operates as a Title II matchmaking platform under the JOBS Act Section 201(c) exemption. We earn on technology and advisory services provided to issuers, never on transaction volume. We have completed 66 engagements since 2016 and charge zero transaction fees to investors, by structure.

Is this a good time to invest in private companies?

Nothing in this article is investment advice. If you are an accredited investor evaluating private markets, the right question is whether the specific opportunity you are looking at has the compliance infrastructure, the data room, and the issuer track record to support a real investment decision. That is what our portal walkthrough covers.

Educational only. Not legal, tax, accounting, or investment advice. Deal Box is not a broker-dealer, placement agent, investment adviser, or custodian. All offerings are issuer-direct and issuer-approved.